If you’ve been struggling to keep up with your mortgage payments and wondering if you’re alone — you’re not. Not even close.

For the past six years, a quiet safety net of Covid-era mortgage rescue programs kept millions of FHA and VA borrowers out of foreclosure. Payment deferrals, forbearance extensions, loan modifications — the tools kept coming, and the foreclosure clock kept getting paused. But those programs have now sunset. The policy changes are in effect. And the bills have finally come due.

In 2026, FHA and VA foreclosure rates are climbing sharply — and Florida is sitting at the center of it.

If you own a home in Fernandina Beach, Amelia Island, Nassau County, or the greater Jacksonville area and you’re behind on your mortgage, this post is for you. Not to scare you — but to make sure you understand what’s happening and what options still exist before the situation moves further out of your hands.

Behind on Your Mortgage? Let’s Talk — Free, Confidential, No Pressure.

A 15-minute conversation could clarify your options and give you a real plan forward.

Why FHA and VA Loans Always Lead the Way in Rising Foreclosures

This isn’t a coincidence or a scandal — it’s structural. FHA and VA loans exist specifically to get people into homes who might not qualify for conventional financing. Lower down payments. More flexible credit requirements. Less cushion built in from day one.

That’s not a criticism of the programs — they’ve helped millions of families achieve homeownership who otherwise couldn’t. But it does mean that when economic pressure builds, FHA and VA borrowers feel it first and feel it hardest. They have less equity to fall back on. Less financial margin. And when the payment relief programs end, the gap between what they owe and what they can afford is often the widest.

We’ve seen this pattern before. We’re seeing it again now.

The Numbers Are Hard to Ignore

Here’s where things stand as of mid-2026:

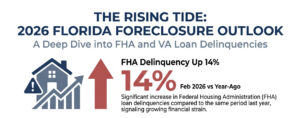

- FHA serious delinquency rates (90+ days past due or already in foreclosure) rose significantly through late 2025 and are now running 14% above year-ago levels as of February 2026.

- Florida consistently leads the nation in new FHA foreclosure starts — a distinction that reflects both our high concentration of FHA loans and the pressures facing our housing market.

- VA loan foreclosure rates hit a decade high as of April 2026 — a milestone that would have been unthinkable during the height of the Covid workout programs.

- Serious delinquency rates for FHA loans are rising sharply compared to conventional mortgages — meaning this isn’t just a rising tide. It’s specifically hitting government-backed loan holders harder.

These aren’t abstract statistics. These are real families in Nassau County, Duval County, and across Northeast Florida who are receiving default notices, opening certified mail they’d rather not read, and trying to figure out what comes next.

What Changed — and Why Now?

The Covid-era mortgage relief machinery was extraordinary in scale and duration. Forbearance programs allowed borrowers to pause payments, sometimes for 18 months or more. Loan modification options were expanded. Foreclosure moratoria kept servicers from moving forward on delinquent loans. And specialized workout programs from FHA and VA gave distressed borrowers path after path to stay in their homes.

Those programs worked — for a while. But they also created a delayed reckoning. The underlying financial hardship for many borrowers never fully resolved. Jobs came back, but income didn’t always keep pace with inflation. Pandemic-era savings were drawn down. And when the workout programs finally closed and servicers returned to standard default servicing procedures, a large pool of borrowers who had been held in a kind of temporary stasis found themselves facing the same payments they couldn’t make — now with added arrears.

Common sense returned to government mortgage default servicing. Unfortunately, for a significant number of homeowners, making the mortgage payment again simply isn’t a reality. And liquidation — meaning the loss of the home — has moved to the forefront.

Important: This is not legal or financial advice. Every foreclosure situation is different, and the right path forward depends on your specific loan type, servicer, timeline, and goals. Always consult with qualified legal and financial professionals before making decisions. What I can offer is real estate expertise — and a honest conversation about your options.

What Options Exist for Homeowners Facing FHA or VA Foreclosure?

Being behind on your mortgage — even seriously behind — does not mean foreclosure is inevitable. It means time matters. The further a default progresses, the fewer options remain. But in most cases, options do exist.

Here are the primary paths I work with homeowners to explore:

Short Sale

A short sale allows you to sell your home for less than what you owe, with the lender’s approval. It’s one of the most commonly used alternatives to foreclosure for FHA and VA borrowers. As a Florida Certified Short Sale Specialist, this is something I guide homeowners through regularly — including VA short sales, which have their own specific process and approval requirements.

A short sale typically results in less damage to your credit than a full foreclosure, and in many cases allows you to avoid a deficiency judgment. The process takes time, which is why reaching out early matters.

Navigating a VA Compromise Sale: Expert Tips for Home-Sellers Facing a VA Loan Short Sale

Deed-in-Lieu of Foreclosure

In a deed-in-lieu, you voluntarily transfer ownership of the home to the lender in exchange for being released from your mortgage obligation. It’s not right for every situation, but for homeowners who have already decided they cannot stay and want to avoid the full foreclosure process, it can be a cleaner exit.

Deed-in-lieu vs. short sale — which is right for you? →

Loan Modification or Repayment Plan

Depending on your servicer and current loan status, some modification options may still be available — particularly for borrowers who have experienced a temporary hardship and can now demonstrate the ability to resume payments. This is worth exploring with your servicer directly, but I’d recommend doing so with a clear understanding of your full situation first.

Traditional Sale (If Equity Exists)

If your home has appreciated and you have equity — even after the mortgage balance and costs — a traditional sale may be your best and simplest option. In some cases, homeowners don’t realize they have more equity than they think. A current home valuation is always worth getting before assuming the worst.

Find out what your home is worth today →

Florida Homeowners: Why Acting Early Matters

Florida is a judicial foreclosure state. That means foreclosures go through the court system — a process that can take 12 to 24 months or longer from first default notice to final sale. That timeline can feel like breathing room. It isn’t — not if you’re waiting to act.

The earlier you engage with your options, the more options you have. Once a foreclosure judgment is entered, the window closes quickly. And once the home sells at auction, it’s over.

I work with homeowners across Fernandina Beach, Amelia Island, Nassau County, and Duval County who are at every stage of the foreclosure process — from the first missed payment to homes already in active litigation. Wherever you are in that timeline, a conversation costs nothing.

Frequently Asked Questions

Are FHA and VA foreclosures really rising that fast in 2026?

Yes. FHA serious delinquency rates are up 14% year-over-year as of February 2026, and VA foreclosure rates hit a decade high in April 2026. The end of Covid-era workout programs is the primary driver. Florida is among the hardest-hit states due to its high concentration of FHA loans.

What’s the difference between an FHA short sale and a VA short sale?

Both involve selling the home for less than the mortgage balance with lender approval, but the approval process, required documentation, and timelines differ between HUD (which oversees FHA loans) and the VA. VA short sales also have specific rules around who can purchase the property. Working with a specialist who knows both processes matters.

Can I do a short sale if I’m already in foreclosure?

In most cases, yes — as long as a final foreclosure judgment has not been entered. The earlier you start the process, the more time you have to work with. Even homes with active lis pendens (foreclosure filed) can often be short sold with the right timeline and lender cooperation.

Will a short sale ruin my credit?

A short sale does impact your credit, but generally less severely than a full foreclosure judgment. The specific impact depends on your credit profile, the lender’s reporting practices, and how the settlement is negotiated. This is something to discuss with a financial advisor — but most homeowners find that a short sale gives them a faster path to financial recovery than a foreclosure on record.

How do I know if I have equity in my home?

Request a current home valuation — which I provide at no cost — and compare it to your current mortgage payoff amount. In today’s market, some homeowners are surprised to find they have more equity than expected, which opens options they didn’t think were available.

You Don’t Have to Figure This Out Alone

If you’re behind on your FHA or VA mortgage in the Fernandina Beach, Amelia Island, or Nassau County area, let’s have an honest conversation about where you stand and what paths are available to you. Free. Confidential. No obligation.

Book Your Free 15-Min Consultation →

Or call directly: 904.601.1192